Let’s use Art Berman’s “thermodynamic economy” premise of how money and energy are related, and then de-construct the Federal Reserve’s assertions about their “infinite” power to prevent global capitalism’s demise.

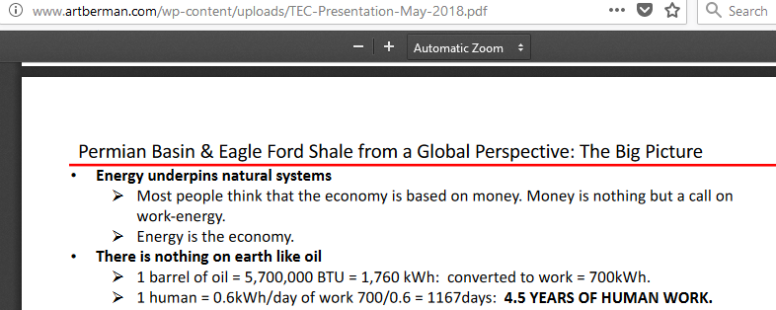

See the first slide: “Most people think that the economy is based on money. Money is nothing but a call on work-energy.”

Now, money is also the means of exchange, and what is used to pay wage-labor for the work we do in creating value, and surplus value for the class of capitalists who employ our labor-power. What economists have “discovered” is that all of the surplus value extracted from labor in the form of large increases in labor productivity since the 1980s, has been clawed to the top ten percent (or less) of the population. The “digital revolution” in the process of production is the source of most of the hyper-productivity of this period. This leaves the U.S. and global working class with stagnant, or steadily falling, real wages. This is the key segment of the growing income and wealth inequality that is now plaguing the U.S. global economic system.

Hold that thought.

“Neel Kashkari, president of the Federal Reserve Bank of Minneapolis, said Sunday night on CBS’s “60 Minutes” that “there is an infinite amount of cash in the Federal Reserve. We will do whatever we need to do to make sure there’s enough cash in the banking system.”

“The Fed actually announced several more measures, but the moves to address the chaos in Treasuries and corporate bonds are likely the most immediately significant. That’s because a look at the debt markets since the collapse of Lehman Brothers Holdings Inc. shows that it’s governmental and nonfinancial corporate obligations that have ballooned in the past decade. So it’s no wonder that they’re responsible for straining the financial system this time around.”

What the Fed is enabling/promoting, is a (future) call on work-energy, sort of a “long-term call option” such as are traded in the vast derivatives markets.

There’s a slight problem with this, however. Approximately 2005 (just before President Cheney rammed thru his Dark Secrets of Fracking legislation thru the Congress), the world was at a point where high-quality energy, that is, cheap petroleum (and natural gas) was becoming short-supply. Best minds to consult on this question are Berman himself, Nate Hagens the long-term “Resilience” contributor, and the Geological Survey of Finland report “Oil from a Critical Raw Material Perspective” by Simon MIchaux (510 pages of it).

In the time of mid-19th century EuroAmerica, when Marx and Engels were working on the “labor theory of value,” at that time, limits to energy supply growth were simply not on anyone’s radar in the field of political economy. They could not have been, because the geophysics of the discovery/deployment of cheap energy sources was still decades ahead. They looked at the “mode of production” or the relations of production as consisting of the property relations of capital and how this impacted the workers of the world.

A 21st-century view of the current economic emergency and the “way out of it” would acknowledge the role of a finite energy supply powering the processes of capital, and the role of two factors: stagnant or falling (real) wages of the workers, plus stagnant incomes to the non-workers (consisting of state-paid social welfare); secondly, the role of huge burdens of debt upon all sectors of societies.

This debt can be said to be, as Berman has further suggested, “a claim on future surplus energy, which does not exist.” The sentence contains the refutation of the claim that the Federal Reserve (or Euro Central Bank, or the Chinese central bank) have “infinite money to throw at the emergency.”

As soon as the public learned that these bailout sequences were NOT going to be infusions of cash, NOR across-the-board mandated wages increases, (that is, actual money which is not more debt) but instead, programs to provide ever more corporate credit (leading to presumably higher paper asset values on the stock market, plus the added insult of using such funds to “buy-back stock” which pushes the paper asset values ever higher)–then the public began to get angry. Very angry. We have a very angry working class now. What we do with the anger is to be seen.

The first half of this decade of the 2020s will consist of the populations of many nations discovering that the emergency isn’t being solved, but instead keeps morphing into further deterioration of the standards of living of the global “non-elite workers” as Gail Tverberg calls us “bottom 90%” of the workers. The second half of this decade will pose the actual crisis of the world energy shocks.

The trigger event for the world energy shocks will be the collapsing of the extraction of United States fracked hydrocarbons, petroleum and natural gas.

So, in summation: No, there is not an “infinite amount of money” available to be deployed to solve the global emergency. Therefore, the emergency will grow and develop according to its own internal dynamics–immune to politicians’ “solutions.”